Family Offices Are Coming out of Their Shell

For the last couple of years, everyone’s been saying, “Capital is gone.”

Except… it’s not.

It’s just showing up in a different way.

Fewer headlines. Fewer big logos. Less drama.

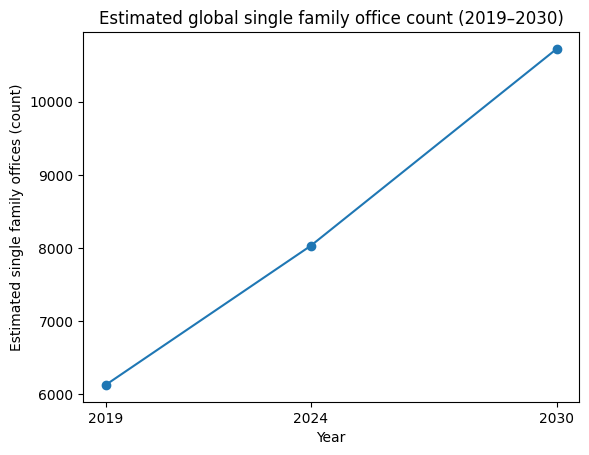

Family offices, especially single family offices, have been growing fast. Deloitte estimates there are about 8,030 single family offices worldwide today, up from around 6,130 in 2019. They project that number could reach 10,720 by 2030.¹

That’s not a small bump. That’s real growth.

Growth of Single Family Offices Globally

And it’s not just more offices. It’s more direct capital. More flexibility. More groups that can actually make decisions without layers of approvals.

Deloitte also estimates that family offices manage about $3.1 trillion today, and that could grow to $5.4 trillion by 2030.¹

That’s serious buying power.

UBS’s Global Family Office Report 2024, which surveyed 320 single family offices representing over $600 billion in wealth, shows that even after shifting allocations in 2023, family offices are still committed to private investments for the long haul.² They aren’t chasing quick wins. They’re thinking long term.

Why the $10MM-$75MM Lane Is Attractive

That middle market range tends to be:

- Big enough to matter

- Small enough to avoid crowded bidding wars

- Often complex enough that speed and flexibility matter more than size

It’s the sweet spot.

Altus Group reported that large deals ($10M+) picked up again in 2025, hitting the highest quarterly count since 2022.⁴ That doesn’t happen if capital disappears. It happens when new buyers step in.

And family offices are stepping in.

Real Estate Isn’t a Real Priority

According to the RBC Wealth Management & Campden Wealth North America Family Office Report 2024:

- 73% of North American family offices invest directly in real estate³

- Real estate makes up about 17% of their overall portfolio³

- Of those investing, 81% focus on residential properties³

So real estate isn’t random for them. It’s a core part of the plan.

And many of these investments are made directly, not just through big funds. That means fewer outside decision-makers, faster calls, and more control.

Family offices like real estate because it’s tangible. It’s long-term. It’s something they can understand and manage.

.png)

Structure Wins in This Environment

Financing conditions help explain why private buyers, including family offices, are competitive again.

Following the 2023 banking disruptions, roughly two-thirds of banks tightened commercial real estate underwriting standards, according to reporting cited by Baker Tilly.⁵

When lending tightens:

- Deals take longer

- Lenders want more certainty

- Creative structures matter more

Family offices have the advantage here. They can:

- Put up more equity

- Hold properties longer

- Move faster

- Structure creatively

- Avoid endless committee meetings

In a market defined now by sidestepping risks, that profile is powerful.

And the numbers are showing, maybe even more powerful than the age-old “big institution” methods.

What This Means

The market hasn't shrunk.

It’s shifted.

The winning offer on a property today may not come from the biggest institution in the room. It might come from the group that can:

- Underwrite calmly

- Structure intelligently and flexibly

- Close without drama

So basically?

Capital didn’t disappear.

It just looks different.

Sources

- Deloitte, The Rapid Expansion of Family Offices and Future Landscape Projections, 2024.

(Estimates of global single family office count and projected AUM growth.) - UBS, Global Family Office Report 2024.

(Survey of 320 single family offices representing over $600B in wealth; allocation trends.) - RBC Wealth Management & Campden Wealth, North America Family Office Report 2024.

(Strategic asset allocation averages; percentage with direct real estate exposure; sector preferences.) - Altus Group, U.S. CRE Investment & Transactions Quarterly Review, 2025.

(Large-deal transaction activity trends.) - Baker Tilly, Commercial Real Estate Debt Dilemma, 2024.

(Commercial bank lending and underwriting tightening statistics.)